4 min 5954

Aave DEFI Introductory Tutorial

Your crypto isn't just collecting dust — it's out there hustling for you. Meet Aave, the DeFi platform that's like a bank, but cooler: no suits, no paperwork, and way better rates. Whether you're parking stablecoins for interest or borrowing against your Bitcoin without a credit check, Aave's got tricks to make your wallet work smarter. Let's break down how it turns "HODLing" into a side hustle.

The "Bank" That Runs on Code (and Your Crypto)

Aave is a decentralized lending app built on Ethereum. Think of it as a financial Lego set: users deposit crypto to earn interest or borrow assets by putting up collateral — all automated by smart contracts. No bankers, no branch hours, and definitely no judgment if you take out a loan at 3 AM.

Why it's a game-changer:

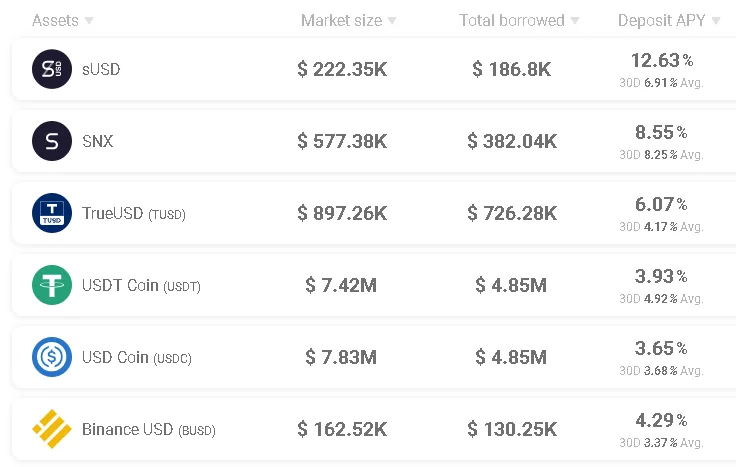

- Passive income made simple: Deposit stablecoins like USDC or DAI and earn up to 8% APY. That's 4x what Chase offers for savings accounts.

- Borrow without begging: Need cash but don't want to sell your ETH? Lock it up as collateral, borrow stablecoins, and pay interest as low as 3%.

- Zero lock-in periods: Unlike banks, you can yank your money out anytime. No penalties, no "please hold for the next representative".

The Aave Vault: Deposits That Actually Do Something

Forget stuffing cash under a mattress. With Aave, your deposits fuel loans for others — and you get paid for it.

How it works:

- You deposit crypto (e.g., USDT, ETH) into Aave's liquidity pool.

- Borrowers use your funds to take out loans, paying interest.

- You earn a cut of that interest, paid in real-time.

Pro tips for max gains:

- Stick to stablecoins for predictable returns (volatility = sleep deprivation).

- Chase "aTokens": Aave's version of deposit certificates. Hold them, and interest auto-compounds in your wallet. Magic? No, just code.

Loans Without the Loan Shark Vibes

Aave's loans aren't for the reckless — they're over-collateralized. Translation: You lock up 150 in ETH to borrow 100 in USDC. Why? To protect the system if prices tank.

Why this rocks:

- No credit checks: Your collateral speaks louder than your FICO score.

Two rate flavors:

Stable: Fixed rates (good for planners).

Variable: Rates shift with market demand (good for gamblers).

Cool hack: Deposit ETH earning 2% APY, borrow USDC at 3%, and use it to buy more ETH. Profit if ETH rises >3%. Risky? Absolutely. But that's DeFi, baby.

Aave's Bonuses and Partnerships

Aave doesn't just sit there — it rolls out perks like a crypto Santa.

- Fee discounts: Take a loan? Pay a tiny 0.25% fee. Better yet, use platforms like Timvi for 12% cashback on fees. Free money alert!

- Safety net: Aave's "Safety Module" lets you stake AAVE tokens to insure the protocol against crashes. You earn rewards for playing hero.

Risks: Because Nothing's Perfect

- Stablecoins aren't always stable: If USDC loses its peg, your "safe" deposit tanks.

- Liquidation nightmares: If ETH drops 50% overnight, your collateral gets sold to cover your loan. Ouch.

- Smart contract bugs: Code is law… until it's hacked.

Aave for Dummies

Q: Is Aave safe?

A: Safer than a piggy bank, riskier than a FDIC-insured account.

Q: Can I get rich with Aave?

A: Not rich, but you'll beat inflation. Maybe buy a nice coffee every month.

Q: What's the minimum deposit?

A: $1. But c'mon, aim higher.

Aave is the DeFi Swiss Army knife: earn interest, borrow flexibly, and dodge bank bureaucracy. Just remember — this isn't Monopoly money. Play smart, avoid greed, and maybe your crypto will finally pay rent.